Long Island ended 2025 as the 40th largest coworking market in the U.S., with 66 coworking spaces following a 3% quarter-over-quarter increase, according to CoworkingCafe’s newly released Q4 2025 U.S. Coworking Industry Report. Nationally, coworking continued to expand through the year’s end, reaching 8,854 locations.

Here’s a closer look at Long Island’s coworking market in Q4 2025:

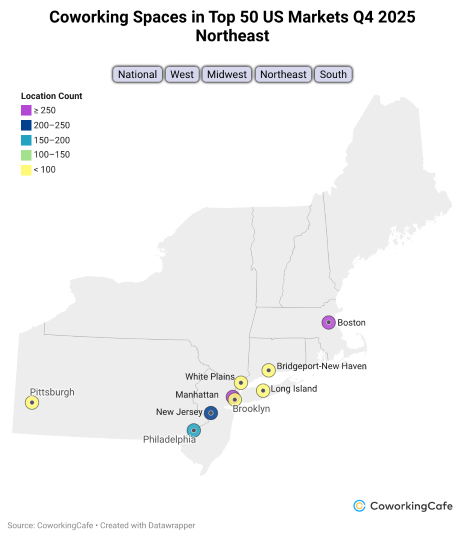

- Inventory growth remains steady: Long Island closed Q4 2025 with 66 coworking spaces, tying it with Cincinnati at #40 nationwide by total inventory. The market expanded 3% quarter-over-quarter and 8% year-over-year.

- Average space size remains well below national levels: Coworking locations in Long Island average 14,546 sq. ft., well below the U.S. average of 18,003 sq. ft. Average size dipped 3% Q-o-Q but is up 14% Y-o-Y.

- Total coworking footprint posts strong annual growth: Long Island’s total allocated flex space reached 0.96 million sq. ft. in Q4, holding nearly flat Q-o-Q (+0.4%) but expanding a notable 23% Y-o-Y.

- Coworking penetration: Flexible office space now accounts for 1.9% of Long Island’s total office inventory, below the national average.

- Top operators: Modern Office Space Long Island (16 locations) leads the local coworking market, followed by Regus (seven locations) and HQ (six locations).

- Pricing trends remain mixed across membership types:

- Virtual offices hold at $150/month, unchanged Q-o-Q and slightly below the $159 national median.

- Meeting rooms dropped to $35/hour (–$10 Q-o-Q), below the $45 national median.

- Day passes increased to $45/day (+$10 Q-o-Q), above the $30 national median.

- Monthly memberships remain at $235/month, unchanged Q-o-Q and above the $220 national median.

National Snapshot:

- The total U.S. coworking footprint grew 4.7% Q-o-Q to 159.4 million sq. ft.

- The number of coworking spaces increased 5% Q-o-Q to 8,854, adding 434 159.4 million sq. ft. net new locations in Q4.

- The average space size edged down just 0.4% Q-o-Q to 18,003 sq. ft., reflecting a continued focus on larger, more versatile hubs.

- Year over year, coworking footprint expanded 16.5% and inventory grew 15%, bringing coworking’s share of U.S. office space to 2.2% by the end of 2025.

- Top operators: Regus remains the national leader, closing Q4 with nearly 1,200 locations across the U.S., followed by HQ (354), Industrious (176) and Spaces (170).

The report leverages proprietary data as of December 2025, analyzing the 50 largest U.S. coworking markets by inventory counts, total and average space size, median pricing and leading operators.

You can find the full report here: https://www.coworkingcafe.com/